What percentage should I contribute to my 401(k)?

What percentage should I contribute to my 401(k)?

What percentage should I contribute to my 401(k)?

Key takeaways

Key takeaways

Empower insight reveals people who set their contribution rate to at least 10% are on track to replace 100% of their working income down the road. If you don’t think you can designate 10% for retirement, review your budget to see if you can free up some extra cash.

Empower insight reveals people who set their contribution rate to at least 10% are on track to replace 100% of their working income down the road. If you don’t think you can designate 10% for retirement, review your budget to see if you can free up some extra cash.

07.26.2022

Contributing to your 401(k) is an important part of retirement planning

You give, and you get.

Your contribution rate is the percentage of your earnings that is deducted from your paycheck and moved into your 401(k) plan or other retirement plan account.

In most cases, you choose the value you want to pitch in.1 And while your take-home pay will be reduced, your retirement nest egg has the potential to grow.

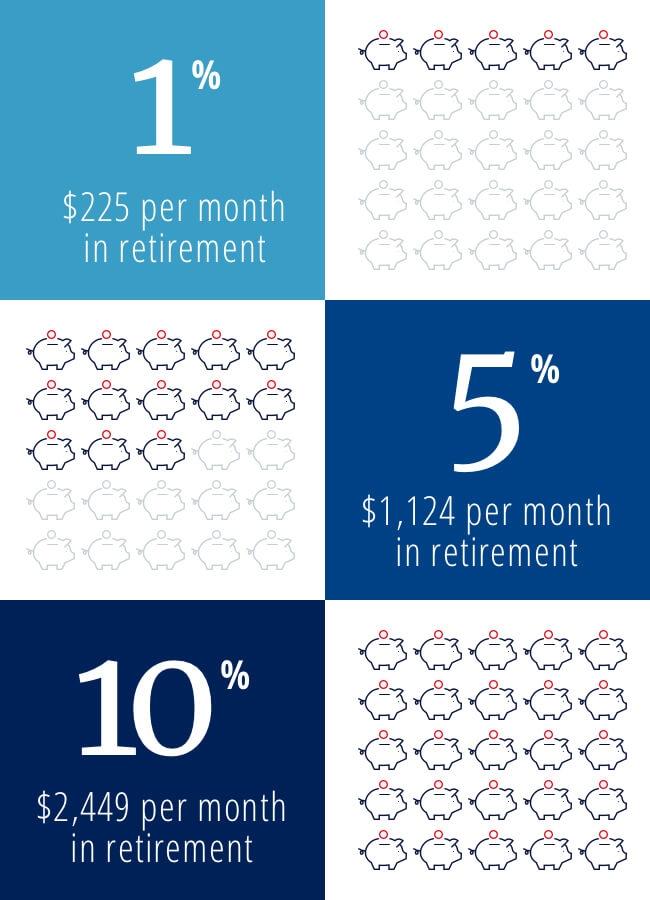

One sound strategy to implement into your retirement savings plan routine is to increase your contribution to 10% (or even more) to your retirement plan account. It can make a big difference, too. Empower insight reveals people who set their contribution rate to at least 10% are on track to replace 100% of their working income down the road.2

When should I start contributing?

The earlier, the better.

If you’re eligible to participate in your employer-sponsored retirement plan, don’t wait to start saving. Even if you can’t afford to set your contribution rate to 10% right away, you can still boost your balance thanks to compound growth potential. With compounding, not only would your investments have the potential to grow, any earnings could also produce earnings because any earnings may be reinvested — tax-free — into your retirement account.

Above all, as you’re climbing the ladder toward 10% as you age, your balance can potentially continue to rise with you.

FOR ILLUSTRATIVE PURPOSES ONLY. This is a hypothetical illustration to show the value of an increase in contributions; it is not intended as a projection or prediction of future investment results, nor is it intended as financial planning or investment advice. It assumes a 6% average annual rate of return, 12 pay periods, $50,000 starting salary with no increases invested over 30 years, a 25% federal income tax bracket, reinvestment of earnings and that the payee lives 20 years in retirement. Rates of return may vary. This illustration does not include any charges, expenses or fees that may be associated with your Program. The tax-deferred accumulations shown above would be reduced if these fees had been deducted

How can I grow my 401(k)?

Little by little, you can make huge strides.

If you want to stay on track for your future, consider increasing your 401(k) contribution by 1% at the beginning of every January until you reach the 10% target. To remain on schedule (and so you don’t forget!), check with your 401(k) provider to see if it offers an automatic escalation feature — which can help you gradually gain ground each year. As Empower research suggests, employees who are in retirement programs with auto-increases are on pace to replace more than 105% of their income in the long run.3

Should I max out my 401(k)?

You don’t have to stop contributing at 10%.

If you max out your 401(k), also known as deferring up to the IRS limit, you can help potentially strengthen your nest egg at an even faster pace. The IRS sets contribution limits on an annual basis when it comes to how much you can save for retirement. In 2022, you can contribute up to $20,500 to your 401(k) plan and in 2023 you can contribute up to $22,500. If you’re age 50 or older in 2022, you may be eligible to sock away an additional $6,500 in catch-up contributions. In 2023 the catch-up contribution limit is $7,500.

What about 401(k) matching?

If your company offers matching, it’s often referred to as “free money.” That’s because when you contribute to your 401(k) plan, many employers will usually match 50% or 100% of your contributions up to a certain amount. For example, if your organization offered a 100% company match up to 5% and you set your contribution rate to 5% (or higher), you would essentially double your total investment when fully vested.

Employer contributions are a great way to boost your overall retirement savings, so a good rule of thumb is to aim to contribute enough to your 401(k) to get the full employer match.

How else can I boost my savings?

If you don’t think you can designate 10% for retirement, review your budget to see if you can free up some extra cash.

Maybe it’s sacrificing your morning mocha, canceling your premium movie channel subscription or bringing your lunch to work throughout the week. Deciding to pass up on a $4 gourmet cup of coffee every day, for example, can put more than $1,000 back in your pocket. If you invested those dollars over a 25-year span, with a modest rate of return, you could total an additional $35,000 for your future.*4

* FOR ILLUSTRATIVE PURPOSES ONLY. This hypothetical illustration is not intended as a projection or prediction of future investment results, nor is it intended as financial planning or investment advice. It assumes an 2% annual rate of return and reinvestment of earnings with no withdrawals. Rates of return may vary. The illustration does not reflect any associated charges, expenses or fees. The tax-deferred accumulation shown would be reduced if these fees were deducted.

1 CNN Business, “Ultimate Guide to Retirement,” October 2020.

2 Empower Institute, “Scoring the Progress of Retirement Savers 2020,” September 2020.

3 Empower Institute, “Success for Savers Through Design or Default: Three ways to encourage better savings habits,” November 2018.

4 Empower Institute, “The Road to Retirement Success: Strategies to decode human nature and improve employee savings,” August 2018.

RO2307366-0722

The content contained in this blog post is intended for general informational purposes only and is not meant to constitute legal, tax, accounting or investment advice. You should consult a qualified legal or tax professional regarding your specific situation. No part of this blog, nor the links contained therein is a solicitation or offer to sell securities. Compensation for freelance contributions not to exceed $1,250. Third party data is obtained from sources believed to be reliable; however, Empower cannot guarantee the accuracy, timeliness, completeness or fitness of this data for any particular purpose. Third party links are provided solely as a convenience and do not imply an affiliation, endorsement or approval by Empower of the contents on such third party websites. Certain sections of this blog may contain forward-looking statements that are based on our reasonable expectations, estimates, projections and assumptions. Past performance is not a guarantee of future return, nor is it indicative of future performance. Investing involves risk. The value of your investment will fluctuate and you may lose money. Advisory services are provided for a fee by either Personal Capital Advisors Corporation ("PCAC") or Empower Advisory Group, LLC (“EAG”) depending on your specific investment advisory services agreement. Both PCAC and EAG are registered investment advisers with the Securities and Exchange Commission (“SEC”) and subsidiaries of Empower Annuity Insurance Company of America. Registration does not imply a certain level of skill or training. © 2023 Empower Annuity Insurance Company of America. All rights reserved. “EMPOWER” and all associated logos, and product names are trademarks of Empower Annuity Insurance Company of America.